Demand for retail area surged to pre-pandemic ranges, with nearly all of the U.S. inhabitants vaccinated and returning to bodily shops and meals and consuming locations, as retail gross sales and whole consumption exceed pre-pandemic peak ranges.

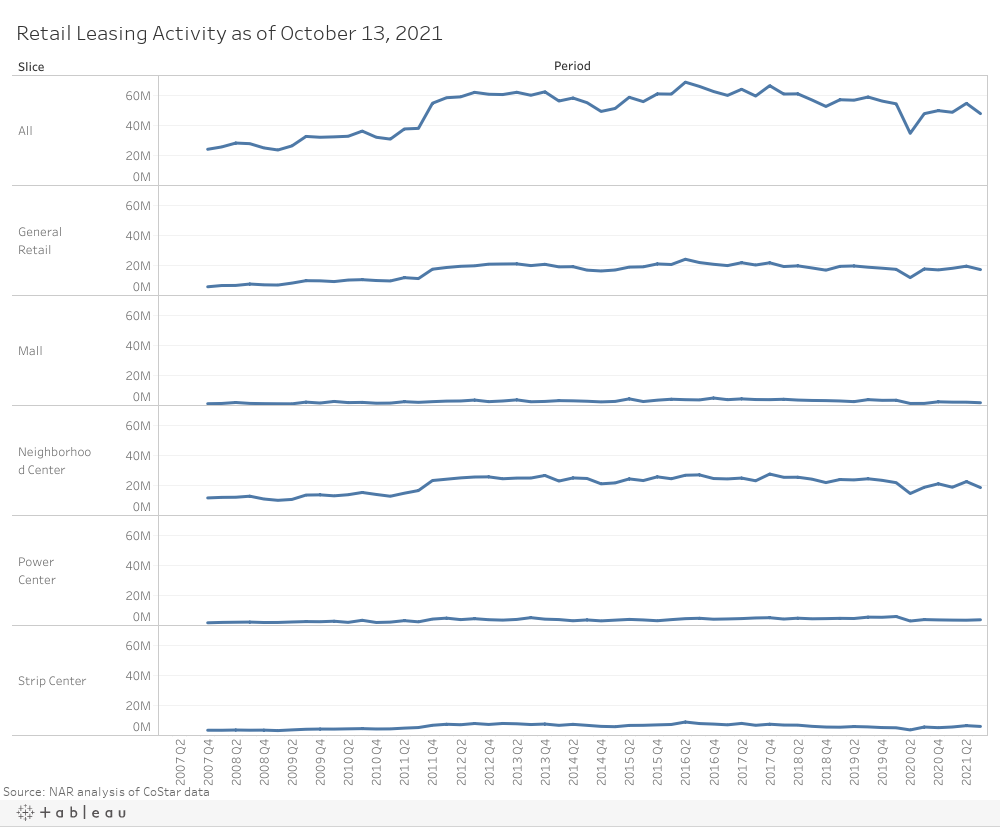

Retail leasing exercise returned to pre-pandemic ranges in Q2 2021. Since that time, as of October 13, retail leasing exercise has softened a bit as exercise totaled 48 million sq. ft, down from 54 million sq. ft in Q2 2021, however nonetheless above ranges noticed the identical interval a yr in the past. As well as, leasing exercise by means of the primary three quarters of 2021 of 151 million sq. ft outpaced that throughout the identical interval final yr (137 million sq. ft). Neighborhood facilities led all property sorts in leasing exercise sq. footage with 18 million sq. ft. 4 markets specifically, Dallas-Fort Value, TX (5 million sq. ft); New York, NY (4.7 million sq. ft); Houston, TX (4.4 million sq. ft); Los Angeles, CA (4.2 million sq. ft); and Atlanta, GA (3.9 million sq. ft), led the nation in retail leasing exercise as of October 13, in accordance with CoStar knowledge. Curiously, nearly all of neighborhood middle leasing exercise sq. footage is within the Southern states and particularly Texas. Dallas-Fort Value, TX and Houston, TX had been the leaders in neighborhood middle leasing exercise with 982,913 sq. ft. and 971,405 sq. ft. respectively.

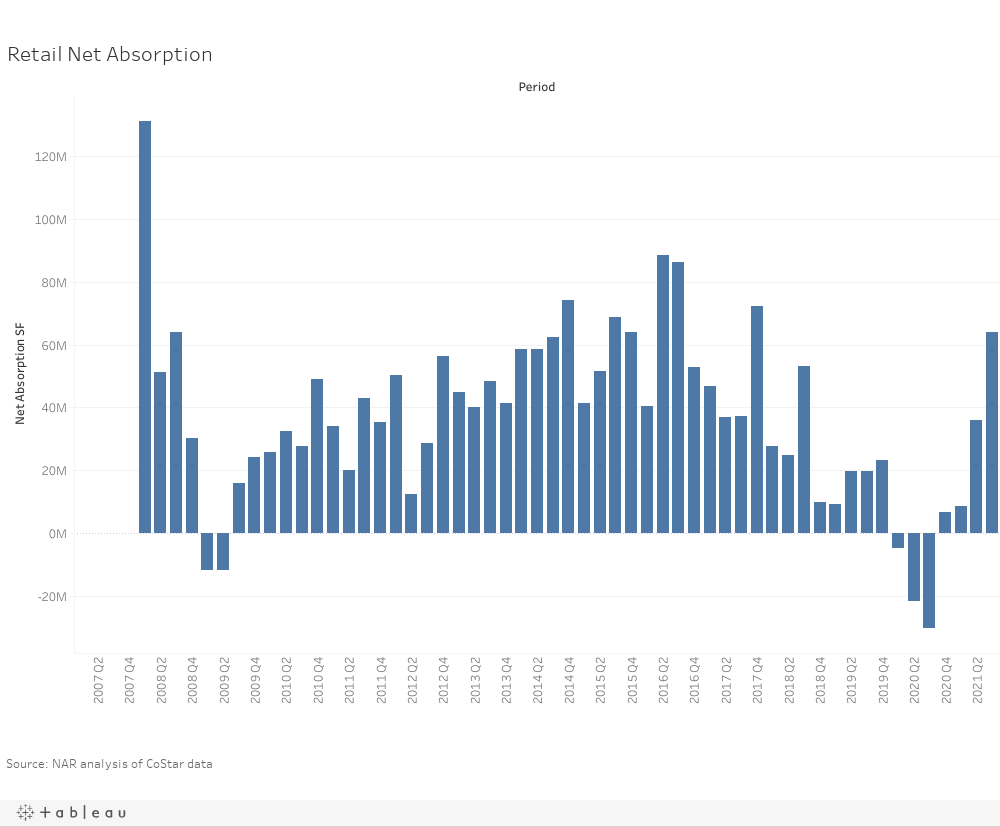

Throughout the previous three months ending October 13, there was a web absorption acquire of 32,158,212 sq. ft, the best stage since This fall 2017. Whereas absorption was constructive throughout all of retail, absorption was constructive for every retail class as properly for the primary time since This fall 2019. Positive aspects in web absorption had been pushed by robust demand for normal retail and neighborhood facilities at 15.9 million sq. ft and 11 million sq. ft respectively.

In accordance with CoStar® market knowledge, main markets resembling Dallas-Fort Value, TX (4.3 million sq. ft) and Atlanta, GA (2.8 million sq. ft) had probably the most constructive retail area web absorption. On the alternative finish of the spectrum, markets which led in detrimental retail web absorption had been Weirton-Steubenville, WV (-431,634); Tulsa, OK (-308,436); Springfield, MO (-306,676); Greeley, CO (-303,840); and New Orleans, LA (-283,202).

With respect to the retail property sorts, Southern states led with probably the most constructive web absorption of every property sort, that’s, normal retail, malls, neighborhood facilities, energy facilities and strip facilities. Texas markets (Dallas-Fort Value and Houston) led the nation in constructive web absorption for normal retail, energy facilities and strip facilities at 1 million sq. ft, 328,054 sq. ft and 299,208 sq. ft respectively.

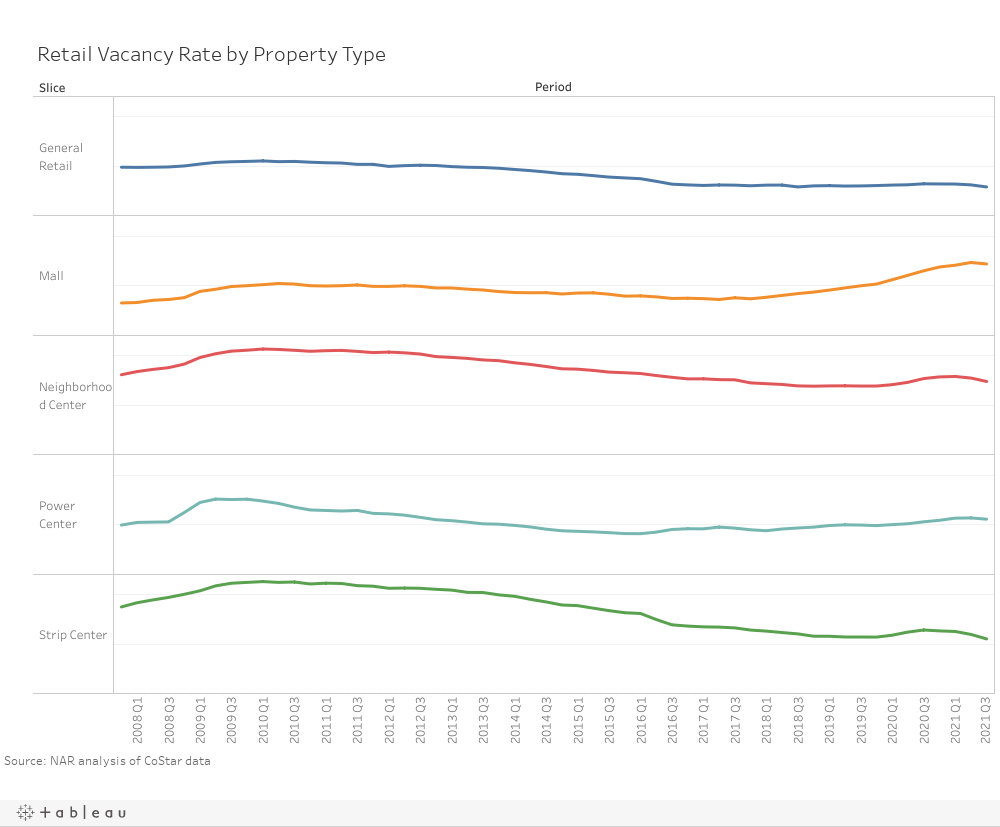

On the nationwide stage, the retail emptiness charge fell 20 foundation factors to 4.8% in Q3 2021, the bottom it has been since Q2 2020, as all retail property sorts exhibited compression. With respect to the retail property classes, neighborhood facilities noticed the best emptiness charge at 7.4% whereas malls, strip facilities, energy facilities, and normal retail had been 7.2%, 5.5%, 5.6%, and a couple of.9% respectively. Strip facilities noticed probably the most enchancment as charges decreased 0.5% from Q2 2021 and decreased 0.9% from the identical interval a yr in the past.

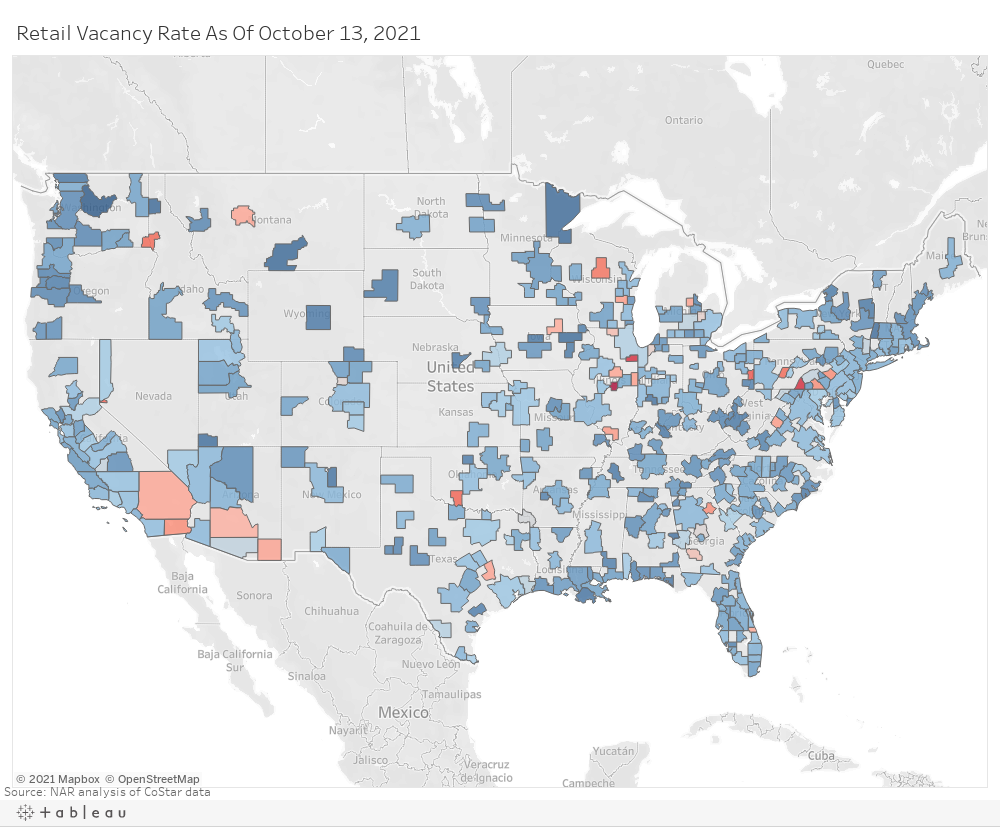

The markets with the best retail emptiness charges had been Decatur, IL (12.4%); Chambersburg-Waynesboro, PA (11%); Kankakee, IL (11%); Carson Metropolis, NV (9.3%); and Johnstown, PA (9.1%), whereas the markets with the bottom emptiness charges had been Billings, MT (1.2%); Coeur d’Alene, ID (1.3%); Duluth, MN (1.3%); and Cedar Rapids, IA (1.3%).

New provide totaled 3.2 million sq. ft in Q3 2021 and is considerably down from 8.3 million sq. ft in Q1 2021 and eight.9 million sq. ft Q2 2021. The brand new retail provide low of Q3 2021 is even decrease than that of Q2 2020, which was 5 million sq. ft. The vast majority of the retail area underneath development stays centered round normal retail.

Retail hire progress is up 1.9% from a yr in the past the place strip facilities have seen probably the most progress at 2.6%, however variations exist in hire shifts by retail property sort and placement. Coastal and concrete metros resembling Boston, MA; Baltimore, MD; and East Bay, CA, have seen detrimental hire shifts for all of retail over the previous 12 months. Conversely, Southern and Midwestern markets like Jacksonville, Atlanta, and Akron are exhibiting the strongest year-over-year hire positive aspects.